An uptick in retail fund flows, the end of the Fed’s rate hikes and a U.S. presidential incumbent seeking re-election are among the positive indicators for equities this year.

When considering the outlook for equities in 2024, investors should reflect first on what happened last year. Those investors with a positive outlook were never truly challenged as equities marched higher throughout 2023. This year will not be as easy. Investors should expect more volatility, and times when an overall bullish view of the market will be in jeopardy. That said, there are five significant reasons to support why 2024 could be another good year for equity investors.

1. Retail Fund Flows Are Up

Historically, after a bear market hits a low point (as the U.S. stock market did in October 2022), it takes about a year of selling before retail investors realize they actually should be buying. Right on time, in November 2023, long-term flows into mutual funds and ETFs turned positive. Based on past investor patterns, this shift is likely to persist. Investors are moving out of money market funds into riskier assets, and some of that money is finding its way into equities.

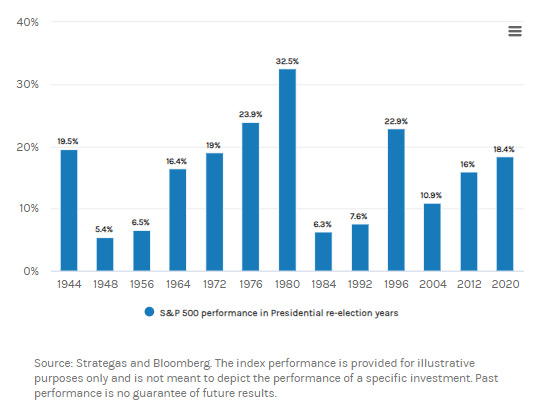

2. An Incumbent Is on the Presidential Ballot

Every time since 1944 that a U.S. president was running for reelection, stocks posted gains for the year. It hasn’t mattered whether the incumbent won—just that there was an incumbent on the ballot. The average one-year return for U.S. equities in those years is 16%, spanning every one of the past 13 instances in which a president was seeking reelection. This makes sense, because presidents can pull levers to help boost the economy, at least over the short term. President Joe Biden certainly has, with spending under the Infrastructure Investment and Jobs Act, the CHIPS Act and the Inflation Reduction Act. As a result, the economy may stay stronger than many people expect.

3. The Fed Is Finished Hiking

Understanding the impact of rate cuts on equity markets is tricky. On one hand, the interval after a string of U.S. Federal Reserve rate increases ends and before the first rate cuts begins is typically a good time for stocks. The gains in the market since the Fed’s final hike in July 2023 are about equal to the average return for stocks historically in such a period. But the Fed isn’t likely to start cutting anytime soon, leaving a window for the market to advance.

The Fed didn’t raise rates to slow an economic cycle but rather to fight inflation. We believe when it does cut rates, it will be declaring victory; it will not be easing because it is spooked by the economy. That’s the reality, and yet pessimists may see rate cuts as a sign of problems with the economy, leading to a pullback for stocks. In this environment, it may take more fortitude to stay bullish and stay invested, but that is still likely to be the right path.

4. Inflation Numbers Are Cooling

Good incremental news on inflation allows the Fed to continue to sound less hawkish, which can help the market. On this point, it’s worth keeping in mind that the monthly consumer price index is measured on a year-over-year basis. Since inflation was running hot all the way through late spring of 2023, inflation numbers should continue to look good for a while, at least compared to where we have been. Later in the year, to be sure, inflation numbers may look less good compared to the prior year, and that might be a negative for stocks.

5. Market Breadth Has Turned Positive

In late Q4 2023, 90% of the stocks in the S&P 1500 index moved above their 50-day moving average, a technical indicator of market breadth (i.e., the overall direction in which stocks are moving) that is bullish for stocks. What this shows is that as investors flipped from selling to buying, as seen in the shift in fund flows at the end of last year, they were looking around for shares of companies that had not already gone up a lot. When we get this signal showing positive market breadth, the S&P 500 Index generally does very well over the next three, six and 12 months. What’s more, the equal-weighted S&P 500 has generally performed even better during a broad market thrust of this kind, and that may be a signal that active managers are likely to outperform.

What to Watch

In this environment, there are two themes that stand out for investment opportunities in 2024.

Value and Growth

While value stocks are, by definition, always cheaper than growth stocks, during recessions they get extremely depressed given investors’ economic fears. Value stocks typically perform very well coming out of recessions, as investors begin to reprice an economic recovery. What’s interesting is that the post-COVID value recovery was very muted. That could be because, in 2023, so many investors expected a “hard landing” in the form of a recession—which has, so far, proven to be inaccurate. Additionally, so much 2024 fiscal spending coming from the Infrastructure Investment and Jobs Act, CHIPS Act and Inflation Reduction Act may also provide an economic boost to these cyclically oriented value sectors, particularly financials and industrials.

At the same time, however, the 2023 recovery began to resuscitate growth stocks following the growth meltdown of 2022. Therefore, investors adding value stocks to their portfolios shouldn’t do so at the expense of growth stocks, where there are plenty of potential consumer discretionary and technology plays.

Investors may want to consider less exposure to defensive sectors: consumer staples, healthcare and utilities. Classically, during the 2022 bear market, investors collectively flocked to dividend-oriented, defensive strategies. This proved the wrong thing to do in 2023, given the stock market recovery. Defensives may underperform again in 2024.

U.S. and Global

Pertaining to U.S. vs. international stocks, one of the biggest mistakes investors have made over the past few years was allocating to other parts of the world away from the U.S. region, because other regions appeared cheaper. Stock valuations, like price-to-earnings ratios, are based on earnings estimates. The most positive earnings revisions have come from the U.S., in particular stocks in the NASDAQ, while some of the worst earnings revisions have come from other parts of the world. In essence, the U.S. has not been as expensive as perceived, and the rest of the world has not been as cheap. That may be the case again in 2024. Therefore, a strategy that includes U.S. and international stocks may continue to outperform one that excludes U.S. equities, even though non-U.S. markets appear cheaper.