American inflation has left its mark across the country’s economy and the world’s financial markets. It has also reared its head between the Golden Arches. Since 1986 The Economist has tracked the price of a McDonald’s Big Mac around the world as a light-hearted guide to the fair value of currencies. Our index shows that the median price of the burger in its home market rose to $5.58 in July, an increase of over 4% since January and 8.3% compared with a year earlier. That is the beefiest rate of American McFlation recorded in our index since July 2012.

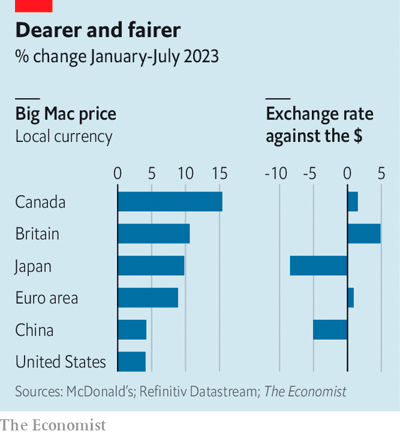

Compared with the rest of the world, however, Americans have escaped lightly. From January to July the price of a Big Mac has risen more than twice as fast in the euro zone and Britain, and nearly four times as fast in Canada (see chart).

What does this mean for the fair value of currencies? According to the theory of purchasing-power parity, a currency’s fundamental value reflects the amount of goods and services it can buy, including burgers. If the price of the Big Mac rises, the currency can buy fewer of them. Its fair value has therefore declined. Since the price of burgers is rising even faster in Europe, Japan and Canada than in America, their currencies’ purchasing power is dropping faster than the dollar’s.

What does this mean for the fair value of currencies? According to the theory of purchasing-power parity, a currency’s fundamental value reflects the amount of goods and services it can buy, including burgers. If the price of the Big Mac rises, the currency can buy fewer of them. Its fair value has therefore declined. Since the price of burgers is rising even faster in Europe, Japan and Canada than in America, their currencies’ purchasing power is dropping faster than the dollar’s.

That is bringing their fair values closer into line with their market values. In January the fair value of the euro, judged by its burger-buying power, was $1.10. That is because €10 could purchase as many Big Macs in Europe as $11 could buy in America. But on the foreign-exchange markets, €10 cost only $10.90. By this measure, the euro looked cheap and the dollar expensive.

That is no longer the case. Thanks to the rise in Big Mac prices in Europe and a small fall in the dollar, the fair value of the euro is now $1.06, less than its market exchange rate. The euro now looks overvalued against the dollar for the first time in two years.

America’s currency is still expensive relative to the British pound and the Canadian dollar, but there is no longer much in it. In fact the euro, the Canadian dollar and the pound now all trade within 5% of the dollar value suggested by the Big Mac index. The greenback looked too expensive to begin with, so America’s weakening exchange rate and its milder inflation, relative to elsewhere, has brought the currency pairs and the fundamentals closer together.

Why had the dollar risen so high? The explanation may lie in another currency-market conjecture: that of “uncovered interest parity”. It says that exchange rates should move to equalise, across borders, the returns to buying safe assets like government bonds. When interest rates rise—as they did more dramatically in America last year than in many rich countries—a currency should first jump, before gradually weakening over time. Bond investors receive a high rate of interest, but suffer a gradual capital loss on the currency. Perhaps that process is now playing out.

This theory also helps explain one of the Big Mac index’s biggest misses this year: its prediction that a dollar should buy only 81 Japanese yen. In fact it buys 142. That suggests the yen is spectacularly cheap, undervalued by 43% against the greenback. The gap is likely to persist until the Bank of Japan feels the need to raise interest rates closer into line with America’s.

That day may not be as far off as investors seem to assume. Last month the central bank unexpectedly tweaked its monetary policy. And even Japan is not immune to McFlation. A Big Mac there costs 9.8% more than it did six months ago.