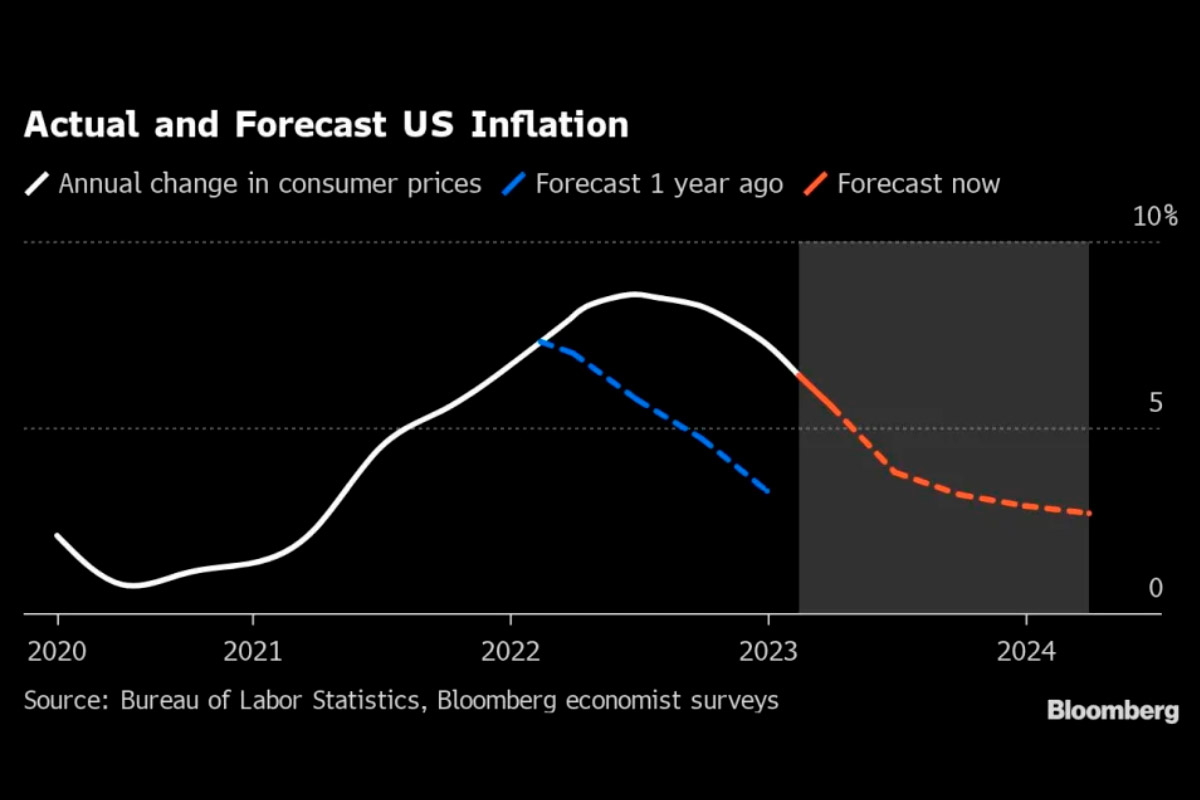

Last year, most US investors and central bankers underestimated how high inflation would climb. Now they may be underestimating how high interest rates will need to go to bring it back down.

In spite of the Federal Reserve’s most aggressive credit-tightening campaign in four decades, the US economy and financial markets started the new year with a bang. Payrolls surged, retail sales jumped and equity prices soared.

Combined with an inflation rate that’s proving sticky and running well above the Fed’s 2% target, that’s a recipe for more rate hikes from central bank Chair Jerome Powell and his colleagues to cool things off.

“There’s a good chance the Fed does more than the markets expect,” said Bruce Kasman, chief economist for JPMorgan Chase & Co.

The risk is that tighter credit eventually catches up with the economy and triggers a recession, as consumers run down the financial buffers they built up during the pandemic. It’s those extra savings – Moody Analytics chief economist Mark Zandi reckons there’s still $1.6 trillion left – and a vibrant jobs market that has allowed households to ride out soaring prices and borrowing costs.

Investors are already upping their bets on how far the Fed will raise rates this tightening cycle. They now see the federal funds rate climbing to 5.2% in July, according to trading in the US money markets. That compares with a perceived peak rate of 4.9% just two weeks ago, and the central bank’s current 4.5% to 4.75% target range.

‘Remain Prepared’

Economists are marking up their estimates of what’s known as the terminal rate — the highest point that the Fed will get to. Deutsche Bank Securities chief US economist Matthew Luzzetti this week raised his forecast to 5.6% from 5.1%, citing a resilient labor market, easier financial conditions and elevated inflation.

Fed policymakers are sounding more hawkish as well.

“We must remain prepared to continue rate increases for a longer period than previously anticipated, if such a path is necessary to respond to changes in the economic outlook or to offset any undesired easing in conditions,” Dallas Fed President Lorie Logan, who votes on rates this year, said on Tuesday.

Cleveland Fed President Loretta Mester, who doesn’t have a vote this year, said Thursday that she saw a “compelling” case for a half-point hike at the last meeting.

During their last forecasting round in December, Fed policymakers penciled in a peak rate of 5.1% this year, according to their median prediction. Fed watchers said they wouldn’t be surprised to see a higher number when the central bank releases new forecasts next month.

“There are significant risks that they will probably continue hiking in the June and July meetings,” said Blerina Uruci, chief US economist at T. Rowe Price Associates. Assuming the Fed also hikes in March and May, as it’s widely expected to, that would take the target range for the funds rate to 5.5% to 5.75%.

Former International Monetary Fund chief economist Ken Rogoff told Bloomberg TV this week that he wouldn’t be surprised if rates end up at 6% to bring down inflation.

‘So Much Better’

Sebastian Mallaby, a senior fellow at the Council on Foreign Relations, wonders if politics may play role in tipping the Fed toward pressing ahead with rate increases this year rather than in 2024, when Americans will be voting for a president.

“If the Fed has got to do some tightening, it’s so much better not to do it in an election year,” he said.

Not everyone is on board with the need for higher rates. Pantheon Macroeconomics chief economist Ian Shepherdson ascribes some of the economy’s early-year strength to warmer-than-normal winter weather, and argues that further hikes would risk an unnecessary recession.

It’s not just the strong January data, though, that has some economists rattled. It’s also data revisions that suggest the jobs market and inflation had more of a head of steam toward the end of 2022 than previously thought.

“Inflation is getting worse,” former White House chief economist and Harvard University professor Jason Furman said in a Feb. 14 Brookings Institution discussion, after news that consumer prices rose by 0.5% last month — up from 0.1% in December.

Furman pegs the underlying inflation rate right now at 3.5% to 4%. While that’s down significantly from six months ago, it’s still well above where the Fed wants it to be.

Another inflation measure, producer prices, rebounded in January by more than expected in the biggest increase since June, according to a report Thursday.

‘Early to Chill’

Powell has declared that the disinflationary process has begun, but he’s also warned that the road back to the Fed’s target will be long and bumpy.

The Fed chair has zeroed in on the labor market as a source of potential inflationary pressure, arguing that demand for workers is outstripping supply and that wages are rising too quickly to be consistent with the Fed’s 2% price goal.

Payrolls have grown an average 356,000 per month over the last three months – well above the roughly 100,000 Powell has said is consistent with equilibrium – while unemployment has dropped to its lowest level since 1969.

Companies have been loath to lay off workers after having had such a hard time staffing up as the economy emerged from pandemic lockdowns. The labor market also faces longer-term structural strains as more and more workers from the huge Baby Boom generation retire.

“It’s very early to say the Fed has any reason to chill,” said Jens Nordvig, founder of Exante Data.